Greece’s battery energy storage (BESS) market is moving rapidly from policy ambition to strategic necessity. After years of strong renewable growth, the Greek power system is increasingly constrained by curtailments, midday price compression, and grid bottlenecks, making storage essential to support further RES integration and system flexibility. At the same time, the market is evolving quickly: auction-based support schemes have started to bring the first projects into operation, while a much larger wave of merchant BESS is emerging under priority grid connection frameworks. The result is a market with strong momentum and significant investor interest, but also with important questions around bankability, regulatory maturity, and long-term revenue visibility. In this context, BESS is becoming not only a technology story, but a strategic test of how Greece will manage the next phase of its energy transition.

Why BESS has become central to the Greek energy transition

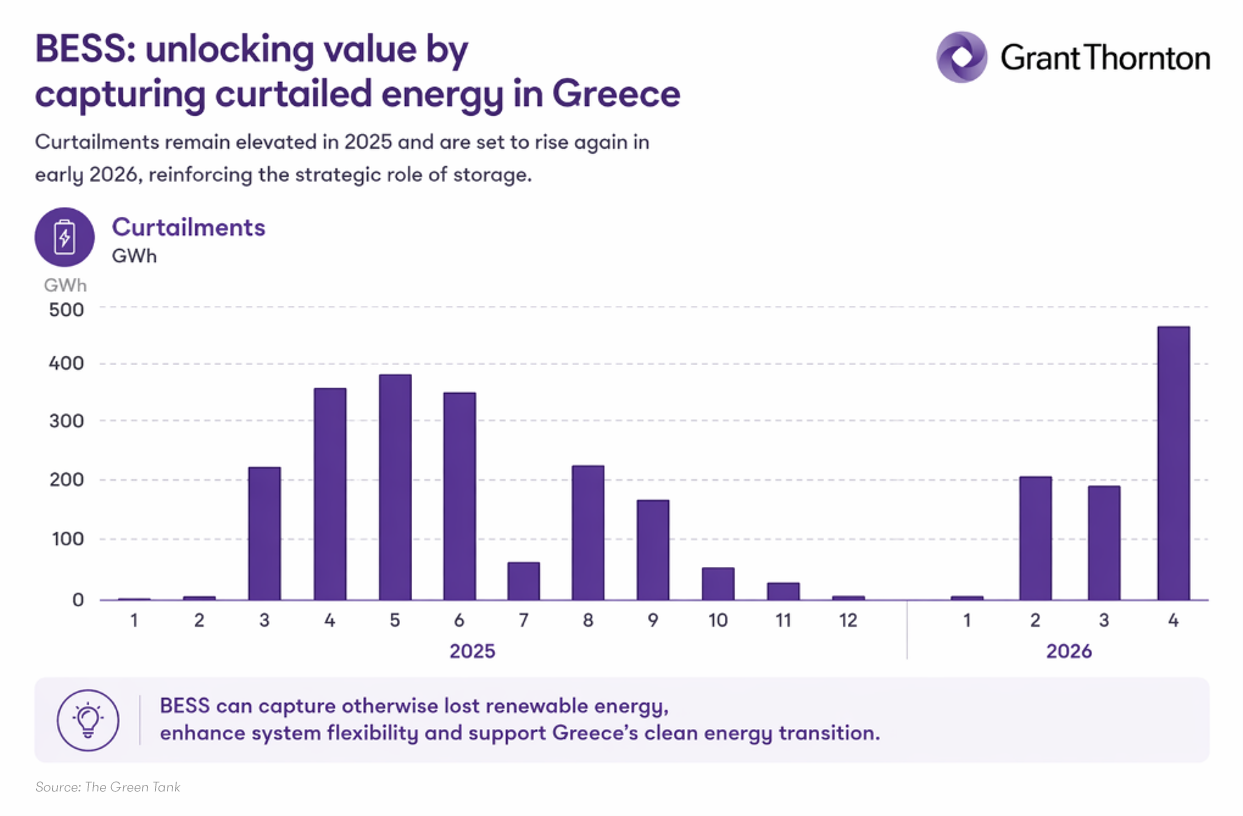

Battery energy storage systems (BESS) have moved to the center of the Greek energy transition because the country’s power system is no longer facing only a renewables growth challenge, but a flexibility challenge too. Greece has expanded renewable capacity rapidly and this success is now exposing structural constraints in the system, including grid congestion, balancing pressures, and increasing renewable curtailments.

![]()

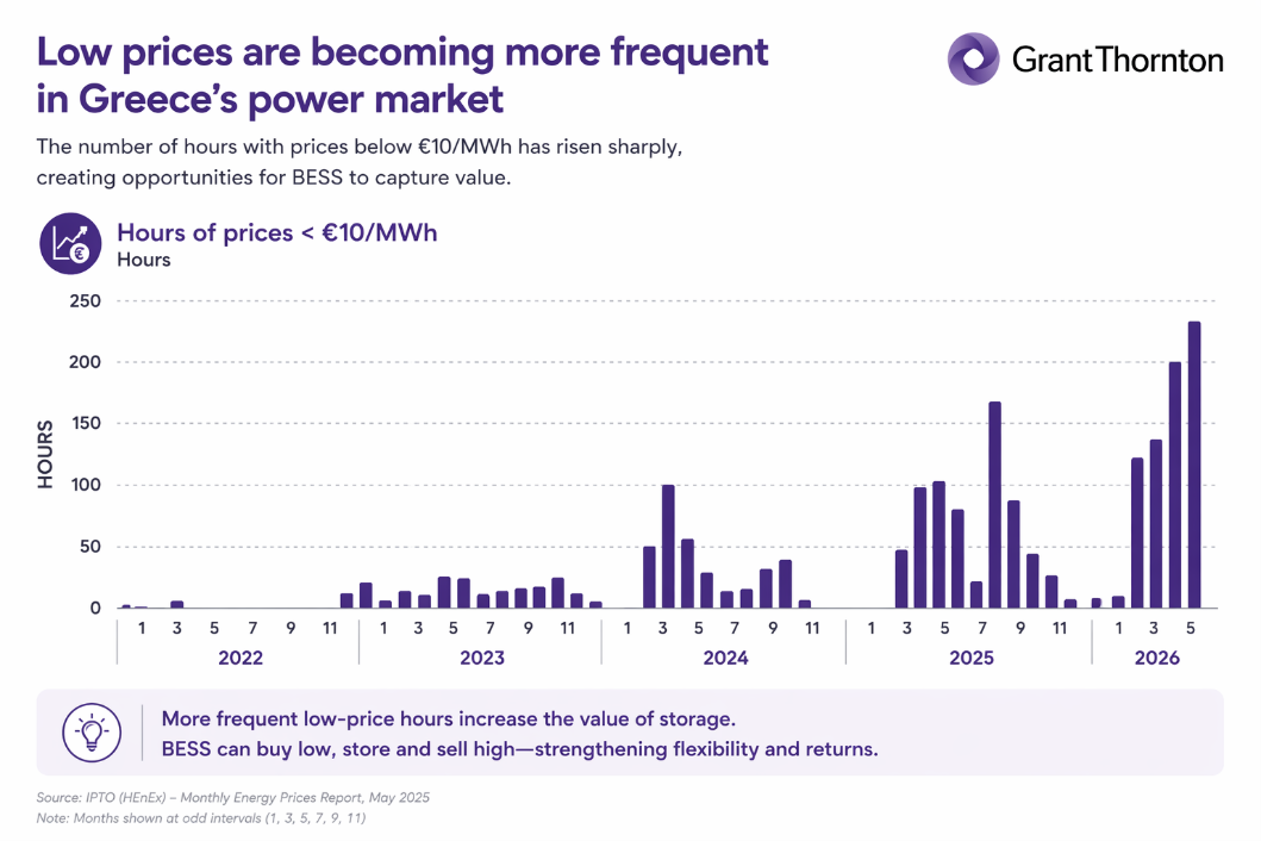

The problem is becoming increasingly visible in market outcomes. Recent reporting indicates that curtailments in Greece have risen sharply, with renewable output increasingly being cut during periods of high solar generation and low demand, while zero or negative wholesale prices are becoming more frequent during midday hours. In this environment, BESS is not simply an additional technology option; it is emerging as one of the main tools available to absorb excess renewable production, shift energy to higher-value periods, and support a system that is struggling to match growing renewable supply with available flexibility.

This is also why the policy and investment narrative around storage has changed so quickly. Greece has already utilized auction schemes to launch its first wave of storage projects, while at the same time opening a much larger pathway for merchant BESS through priority grid connection regimes. The scale of investor interest has been substantial, with applications for merchant battery projects far exceeding the capacity targeted under the new framework. Taken together, these developments suggest that BESS is becoming central not only because the system needs more storage, but because the country now needs storage to preserve the economic value of further renewable growth and to make the next phase of its power market transition workable.

![]()

Policy evolution: From subsidized BESS to merchant BESS

The development of battery storage in Greece has reasonably not followed a purely market-driven path from the outset. Instead, it has evolved through a staged policy approach in which the first objective was to launch the sector through public support and create an initial set of operating reference projects before moving toward wider commercial deployment. This sequencing is important because it helps explain both the current momentum of the market and the tensions now emerging around bankability and implementation.

The first phase of the Greek BESS framework relied on state support mechanisms designed to reduce early investment risk. The initial standalone battery auctions combined capital support with operational support through long-term contracts, helping to create the first generation of utility-scale projects in a market that still lacked mature storage revenues. The regulator utilized grants and support mechanisms precisely because electricity markets did not yet fully monetize the value of storage, making early public support necessary for market entry.

A second phase then began to emerge, marked by a clear policy shift toward merchant deployment. Greece introduced a new merchant BESS priority regime that gives standalone battery projects priority in receiving final grid connection offers while expecting them to operate on market revenues rather than subsidy support. This framework is a fundamental move toward merchant storage and part of a broader strategy to accelerate deployment while reducing curtailments and improving grid stability.

Priority Access Replaces Direct Support

This shift is strategically important because it changes the role of the state. In the first phase, public support was used to create the market. In the second phase, the state is increasingly acting as an enabler of access—particularly through priority connection—while transferring more revenue risk to private investors. This is a transition from subsidy-backed development toward fully merchant models, with priority grid access replacing direct revenue support as the main policy catalyst.

At the same time, the move toward merchant BESS does not mean that the market has become fully mature. Although the policy direction is now more market-based, major questions remain around financing, ranking criteria, operational rules, and long-term revenue visibility. In that sense, Greece is entering a more advanced phase of BESS development, but not yet a fully de-risked one. The policy framework is evolving faster than the financial and commercial frameworks that would normally underpin a stable merchant market.

The rise of hybrid assets

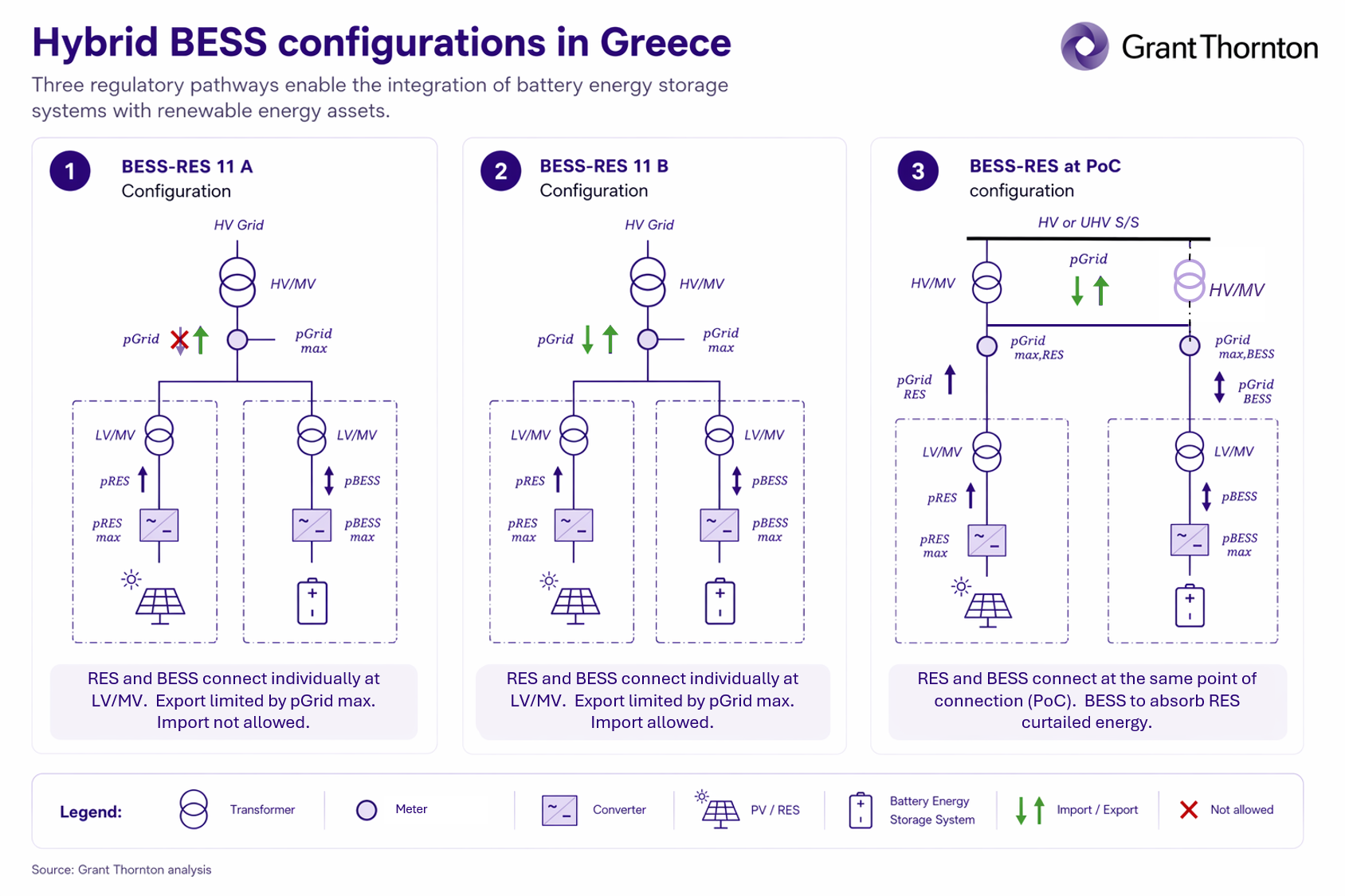

As the Greek market moves from a phase of rapid renewable build-out to a phase of system integration, hybrid assets are emerging as one of the most strategically important developments in the BESS space. Curtailments, low midday prices and growing grid constraints are making standalone renewable projects more exposed, while also increasing the value of storage as a complementary asset. In this context, combining renewable generation with batteries is increasingly seen not simply as a technical enhancement, but as a way to improve the economic resilience of new projects.

The logic behind hybridization is straightforward. In a system where solar output is often concentrated in low-value hours, a co-located battery can absorb part of that surplus generation and shift it to periods of higher demand or stronger prices. Co-location with renewable generation is emerging as one of the most effective ways to stabilize battery economics while improving the capture rates of solar and wind assets. When a battery is paired with a solar plant, it can convert otherwise-curtailed generation into more bankable revenue while also relieving pressure on the local grid.

![]()

This makes hybrid assets particularly relevant in Greece, where curtailment is becoming more structural and increasingly affects project economics. Μany investors and some banks are now pairing PV projects with energy storage specifically to create new revenue streams and mitigate the impact of curtailments and zero-price periods. In fact, the financial pressure on standalone solar assets is already material, reinforcing the commercial case for hybridization.

Hybridization as a Strategic Response

Hybrid assets also fit the broader strategic direction of the Greek market. A shift from a market focused primarily on adding renewable megawatts to one that is now prioritizing flexibility, dispatchability and system value is evident. In that environment, projects that combine generation and storage are better aligned with the needs of the power system because they can offer a smoother and more controllable profile than standalone intermittent generation.

For developers and investors, the rise of hybrid assets also changes how project strategy should be approached. The focus is no longer only on securing a permit and a connection point for a standalone plant; it is increasingly about optimizing the combined value of generation, storage, grid access and market participation. In practical terms, this means that the competitiveness of future projects in Greece may depend not only on the quality of the renewable resource, but on how effectively storage is integrated into the overall asset design. In a market where both curtailment and merchant exposure are rising, hybridization is becoming one of the clearest strategic responses to the next phase of the Greek energy transition.

Market dynamics: strong interest, but uneven visibility on realization

The Greek BESS market is attracting very strong investor interest, but the scale of announced ambition should not be confused with the scale of projects that will ultimately be financed, built and operated. Applications for merchant standalone battery projects have far exceeded the capacity that Greece intends to accommodate under the new priority regime.

This is a sign of strong confidence in the long-term strategic role of storage in Greece, but it also reflects the fact that project applications are being made in a market that is still sorting out some of its most important commercial parameters. There is lingering uncertainty over ranking criteria, grid connection conditions, and the detailed operational framework for storage participation. In that sense, the market is energetic and crowded, but not yet fully settled.

Another important feature of current market dynamics is the distinction between pipeline growth and actual market entry. Although Greece has already run supported tenders and created a large merchant pipeline, only a limited amount of BESS capacity has actually entered the Greek electricity market by early 2026. The first battery energy storage systems were integrated into the day-ahead and intraday markets only recently, while implementation delays have slowed down the effective participation of storage projects that have already progressed through earlier support schemes.

This gap between pipeline and operation matters because it highlights the difference between strategic momentum and bankable execution. A market can generate a large volume of applications when the directional policy signal is positive, especially if priority grid access is available, but the conversion of that pipeline into live assets depends on much more than policy intent. In fact, financing hurdles, operational uncertainty and unresolved implementation details continue to shape the real delivery outlook for many projects.

Risks to the development of the BESS sector

Despite the strong growth momentum observed in recent years, the long-term development of the Greek battery energy storage sector is not without challenges. While the market has benefited from a supportive regulatory framework, increasing renewable energy penetration and growing investor interest, several risks could affect the pace of deployment, project economics and the overall sustainability of the sector.

![]()

Revenue cannibalization and market saturation

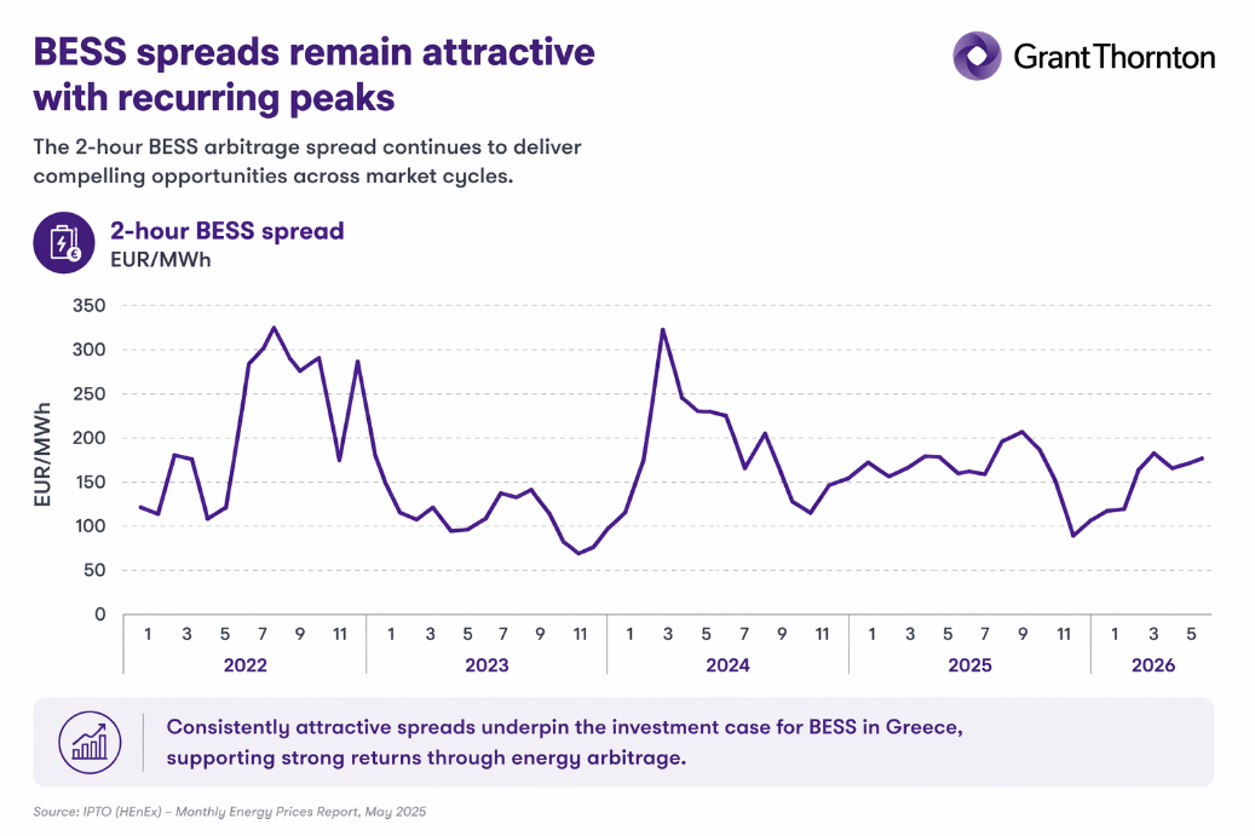

The most significant long-term risk facing the Greek BESS market is the progressive cannibalization of storage revenues as installed battery capacity increases. The current investment rationale for standalone storage projects relies heavily on arbitrage opportunities in the Day-Ahead and Intraday Markets, as well as participation in the Balancing Market. However, as more storage assets enter operation, competition for the same revenue streams will intensify, gradually reducing price spreads and balancing market opportunities. This phenomenon has already been observed in more mature storage markets, including the United Kingdom and certain regions of Australia, where rapid deployment of battery projects has led to declining ancillary service revenues and lower merchant returns. Greece is expected to follow a similar trajectory as the cumulative installed storage capacity increases over the coming years.

![]()

Regulatory and market design risk

Although Greece has established a robust regulatory framework for battery storage, the market remains relatively young. Future changes in balancing market design, network charging arrangements, flexibility mechanisms, congestion management frameworks or revenue support schemes may affect project economics. Furthermore, the interaction between storage participation in wholesale markets, balancing markets and future flexibility or capacity markets remains under development. Regulatory uncertainty regarding the long-term treatment of storage assets may increase investor caution, particularly for projects relying on merchant revenues.

Grid connection and network constraints

The rapid increase in applications for both renewable generation and storage projects is creating growing pressure on the transmission and distribution networks. Delays in grid connection works, reinforcement requirements and limited network hosting capacity may affect project development timelines and increase capital expenditure requirements.

Merchant price volatility

Battery storage projects are highly exposed to wholesale market dynamics. Future electricity prices will be influenced by multiple factors, including renewable energy deployment, fuel prices, interconnection developments, demand electrification and broader European market conditions. Investors therefore face uncertainty regarding the long-term evolution of merchant revenues.

Technology and performance risk

Although lithium-ion battery technology has become increasingly mature, investors remain exposed to performance-related risks, including accelerated degradation, availability issues, replacement costs and evolving technology standards. Project economics are particularly sensitive to assumptions regarding battery degradation rates, operational cycling strategies and future augmentation requirements. Any deviation from expected performance may materially affect project returns.

Financing and cost of capital risk

The viability of merchant storage projects depends heavily on financing conditions. Rising interest rates, tighter lending requirements or changing risk perceptions among financial institutions may increase project costs and reduce investment attractiveness. As the market transitions from subsidized projects to merchant-based business models, lenders are expected to place greater emphasis on revenue certainty, contractual arrangements and stress-tested financial projections.

Taken together, these risks suggest that the development of the Greek BESS sector is likely to be shaped not only by the size of the pipeline, but by the quality of risk allocation across policy, markets and financing structures. The strategic challenge for Greece is therefore not simply to approve or encourage more battery capacity, but to ensure that the commercial and regulatory environment is stable enough for that capacity to be delivered at scale. Without that, the market could remain characterized by strong interest and large application volumes, but a much narrower set of projects that actually become operational.

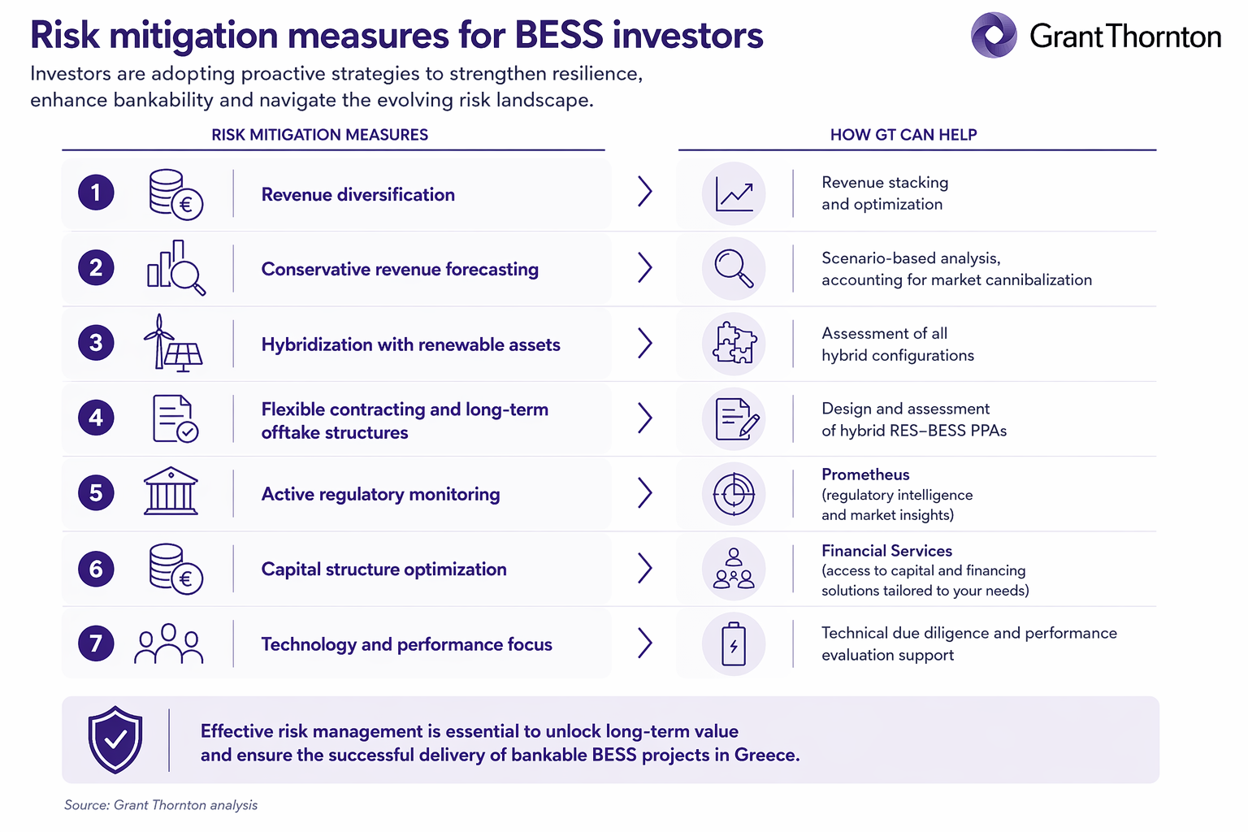

Risk mitigation measures for BESS investors

In response to the evolving risk landscape, investors are increasingly adopting sophisticated strategies to enhance project resilience and improve the bankability of storage assets. The most successful market participants are moving away from pure merchant exposure and developing diversified revenue and risk management approaches.

![]()

Revenue diversification

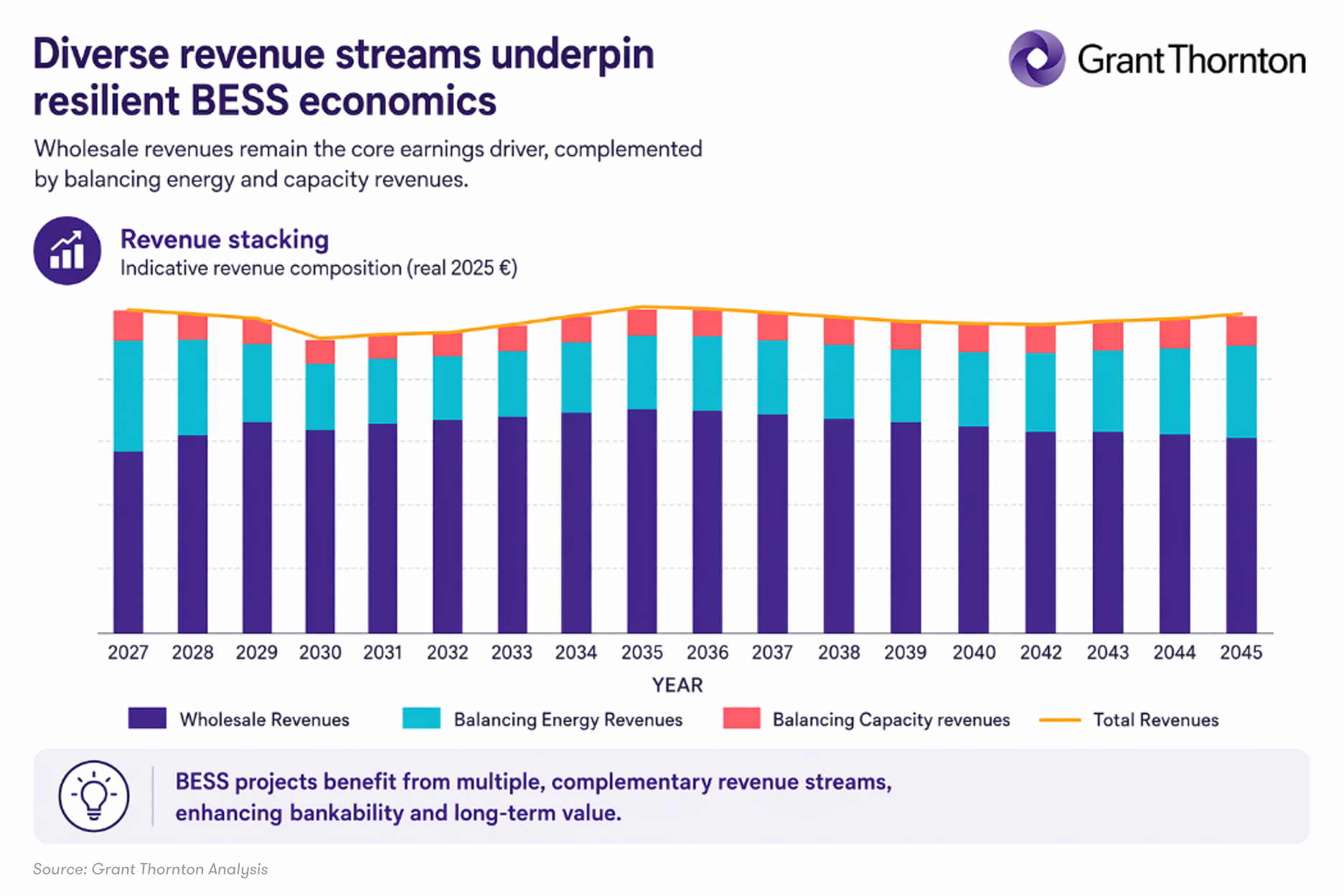

A key mitigation strategy involves maximizing revenue stacking opportunities across multiple market segments. Rather than relying on a single source of income, investors seek to combine revenues from wholesale arbitrage, balancing services and future ancillary services products. Diversified revenue portfolios reduce dependence on individual market mechanisms and improve the resilience of project cash flows.

![]()

Conservative revenue forecasting

Investors and lenders are increasingly applying conservative assumptions regarding future market revenues, particularly in relation to balancing market income. Long-term business plans are progressively incorporating assumptions regarding revenue cannibalization and declining market spreads as storage penetration increases. Scenario-based modelling and sensitivity analysis have become standard practice in investment decision-making processes.

Hybridization with renewable assets

The co-location of storage with solar and wind generation is emerging as an important risk mitigation strategy. Hybrid projects can improve asset utilization, reduce curtailment exposure, enhance renewable energy capture and create additional value through optimized dispatch strategies. As renewable curtailments increase in Greece, hybrid configurations are expected to become increasingly attractive from both commercial and regulatory perspectives.

Flexible contracting and long-term offtake structures

Although storage projects traditionally operate on a merchant basis, investors are increasingly exploring contractual mechanisms that can provide partial revenue certainty. These include capacity agreements, flexibility service contracts, tolling arrangements and structured offtake agreements with utilities, suppliers or large consumers. Such arrangements can improve financing conditions and reduce exposure to short-term market volatility.

Active regulatory monitoring

Given the evolving nature of the storage regulatory framework, investors increasingly maintain dedicated regulatory monitoring processes and engage proactively with market consultations and industry associations. Early identification of regulatory developments enables investors to adapt commercial strategies and investment plans before changes are implemented.

Capital structure optimization

Investors are also focusing on financial resilience through prudent leverage levels, diversified financing sources and the maintenance of adequate liquidity reserves. As storage markets mature, financial flexibility will become an increasingly important competitive advantage, particularly during periods of market adjustment and revenue compression.

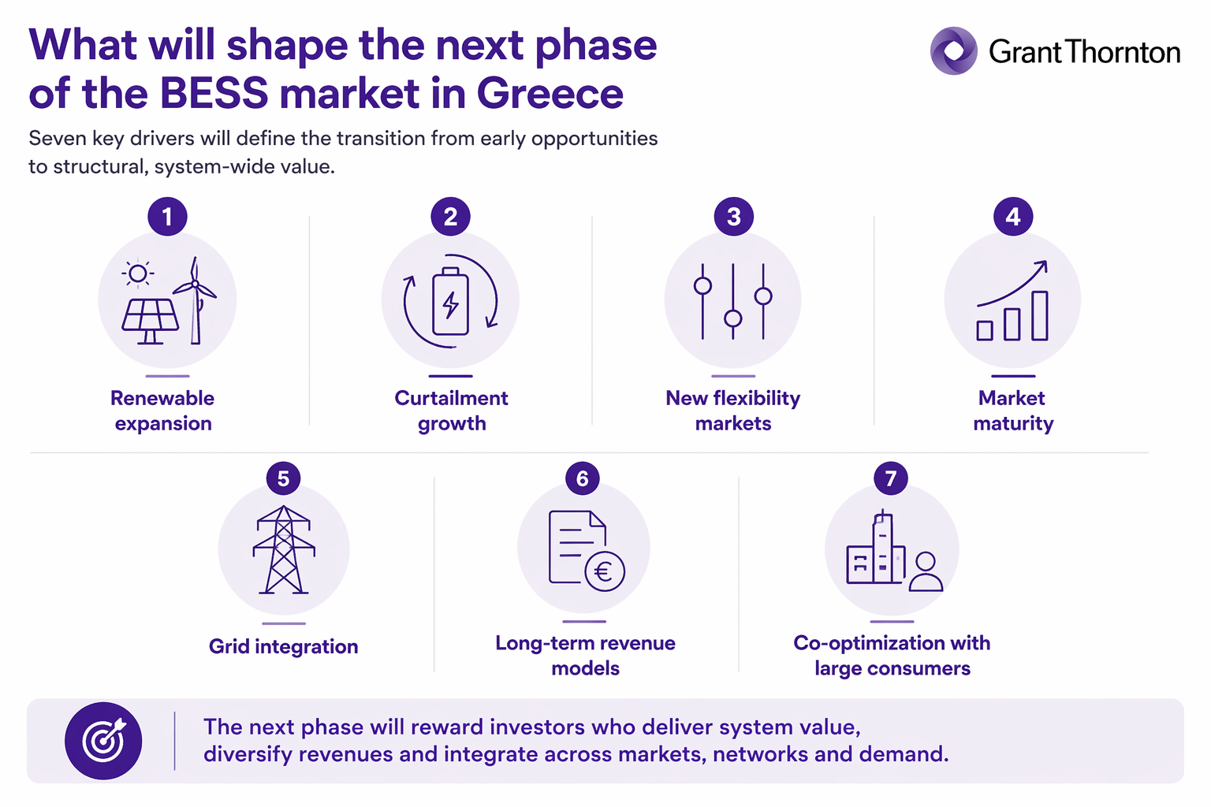

Outlook: What will determine the next phase of the BESS market in Greece

![]()

The Greek BESS market has successfully completed its initial phase of development, characterized by regulatory establishment and early investment activity. The next phase will be considerably more complex and will require storage assets to deliver value across multiple dimensions of the electricity system. Ultimately, the future success of the sector will depend on its ability to evolve from a balancing market opportunity into a core infrastructure solution that supports renewable integration, network optimization, system flexibility and long-term security of supply. Investors that position themselves around these structural drivers rather than short-term market opportunities are likely to be the ones that benefit most from the next chapter of Greece's energy transition.

The scale of renewable energy penetration

Perhaps the most important driver of future storage demand will be the continued expansion of renewable energy generation. Greece has established ambitious renewable energy targets for 2030 and beyond, with solar photovoltaics expected to play a dominant role in future capacity additions. As renewable penetration increases, the power system will experience greater intraday price volatility, more frequent congestion events and higher levels of renewable curtailment. These conditions create a growing need for flexible resources capable of shifting energy across time, supporting system balancing and maximizing the utilization of renewable generation. The long-term outlook for storage therefore remains fundamentally linked to the pace at which renewable generation continues to expand.

The emergence of curtailment as a system-wide challenge

A defining characteristic of the next phase of the Greek electricity market is likely to be the increasing importance of renewable energy curtailments. As renewable capacity grows faster than network infrastructure and system flexibility, periods of excess generation are expected to become more frequent. In this environment, battery storage will increasingly derive value not only from traditional arbitrage opportunities but also from its ability to capture energy that would otherwise be curtailed. This dynamic is likely to accelerate the development of hybrid renewable-storage projects and encourage the integration of storage directly within renewable portfolios. The evolution of curtailment management frameworks and compensation mechanisms may therefore become a critical determinant of storage investment decisions.

The development of flexibility markets

The introduction of flexibility provisions within the Greek distribution framework represents a potentially transformative development for the sector. As distribution network operators increasingly seek alternatives to conventional network reinforcement, storage assets may gain access to entirely new revenue streams linked to congestion management, voltage support and local network services. Although these markets remain at an early stage, their successful implementation could significantly diversify storage revenues and reduce reliance on balancing market income. The speed with which flexibility markets are designed, implemented and scaled will therefore play an important role in shaping the future economics of storage projects.

Revenue cannibalization and market maturity

The next phase of the market will also be defined by how successfully investors adapt to increasing competition. The rapid deployment of battery projects inevitably leads to revenue cannibalization, particularly in balancing markets where storage technologies are often the most competitive providers of flexibility. As installed storage capacity increases, future project success will depend less on access to a specific revenue stream and more on the ability to optimize across multiple markets simultaneously. Sophisticated trading strategies, advanced forecasting capabilities and portfolio optimization tools are likely to become increasingly important sources of competitive advantage. The transition from a high-margin emerging market to a mature infrastructure sector is already beginning.

Network infrastructure and grid integration

The ability of transmission and distribution networks to accommodate large volumes of storage capacity will significantly influence future deployment rates. Grid connection timelines, reinforcement requirements and network hosting capacity will increasingly shape project economics and development schedules. At the same time, storage itself may become part of the solution to network congestion. The extent to which regulators enable storage to participate in congestion management and network optimization mechanisms will determine whether batteries are viewed solely as market assets or as critical infrastructure supporting the energy transition.

The evolution of long-term revenue models

One of the key questions facing the sector is whether storage revenues will remain predominantly merchant-based or whether longer-term contractual arrangements will emerge. International experience suggests that mature storage markets tend to evolve towards a combination of merchant revenues and contracted income streams, including flexibility services, capacity mechanisms, network support contracts and long-term agreements with utilities or large consumers. The emergence of such revenue stabilization mechanisms would significantly enhance bankability and could unlock a new wave of institutional investment in the sector.

Co-optimization with large electricity consumers

The growing interest in data centers, industrial electrification and large-scale electricity consumers presents another important opportunity for the storage sector. As electricity demand becomes increasingly concentrated in large, highly reliable loads, storage may play a critical role in managing procurement costs, enhancing resilience and facilitating renewable energy sourcing strategies. The interaction between storage, corporate PPAs and large electricity consumers could become one of the most important commercial developments of the next decade.

Conclusions

Greece is quickly emerging as one of the most strategically important battery storage markets in Southeast Europe, not because storage is a peripheral addition to the energy transition, but because it is becoming essential to making high renewable penetration workable in practice. Recent market experience shows a system under increasing pressure from curtailments, price compression and grid constraints, while at the same time policy has moved decisively from early support schemes toward a much larger market-oriented storage model.

This creates a market of real opportunity, but also one of real complexity. Strong investor interest and a rapidly expanding pipeline confirm that BESS is now central to Greece’s next energy chapter, yet the path from application to operation remains shaped by revenue uncertainty, implementation risk and financing discipline. In that sense, the future of the sector will not be determined only by how many battery projects are announced, but by how effectively Greece can align regulation, grid development and commercially viable business models.

Ultimately, BESS in Greece is no longer just a technology story; it is a test of whether the country can move from renewable expansion to system optimization. The projects that succeed will be those that combine sound asset strategy, strong market positioning and realistic risk management in a fast-changing regulatory and commercial environment.

Related Services

We work at an impressive pace. Yours. Discover how: