The oil crisis of 1973

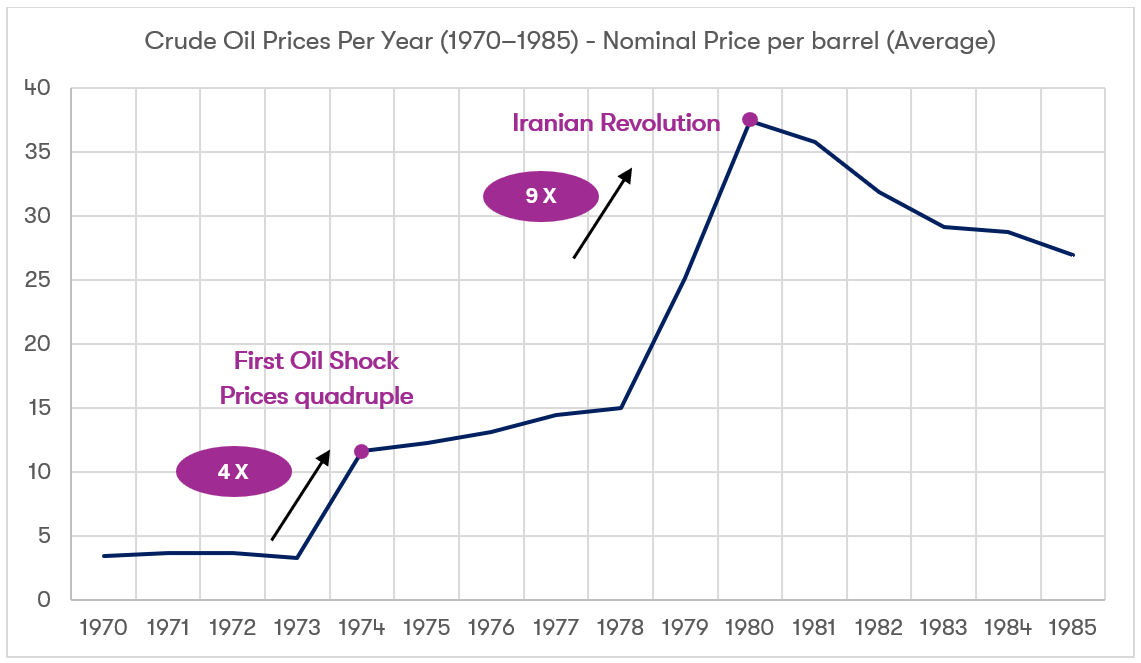

Among the most defining episodes in this history is the 1973 oil crisis, that reshaped energy policy, economic planning, and international relations. In October 1973, members of the Organization of Arab Petroleum Exporting Countries (OAPEC) imposed an oil embargo on nations perceived to support Israel during the Yom Kippur War. Within months, the global price of crude oil quadrupled, rising from approximately $3 per barrel to nearly $12 per barrel, as illustrated in Figure 1. The immediate economic consequences were severe: inflation surged in Western economies, industrial production slowed, and the balance of payments for oil-importing nations deteriorated rapidly. Countries with heavy reliance on imported petroleum, including Japan, the United States, and most of Western Europe, were forced to re-evaluate not only their energy policies, but also the resilience of their entire economic infrastructure.

![]()

Figure 1: Crude Oil Prices Per Year (1970–1985) - Nominal Price per barrel (Average)

The 1973 crisis revealed, perhaps more vividly than any prior event, the systemic vulnerability embedded in the concentration of energy supply routes and production. Similarly, the Strait of Hormuz, a narrow maritime chokepoint connecting the Persian Gulf to the Gulf of Oman and the Arabian Sea, emerged as a symbol of strategic fragility. Approximately 20% of global oil flows today, and a similar proportion in 1973, pass through this strait, making it one of the world’s most critical arteries for energy transportation. Any disruption - whether due to conflict, political sanction, or technical blockade - has the potential to trigger immediate global price shocks, as was partially witnessed during periods of tension in the late 1970s and in the 2010s. The concentration of supply, coupled with the lack of viable alternative routes for crude oil from the Persian Gulf, underscored the need for both geopolitical foresight and strategic stockpiling.

Policy Response: Diversification and Coordination

Following the 1973 shock, industrialized nations adopted a multi-faceted approach to enhance energy security. The International Energy Agency (IEA) was established in 1974 to coordinate oil stockpiling, demand management, and collective response mechanisms among member states. Strategic petroleum reserves became a policy cornerstone: the United States, for instance, began accumulating reserves sufficient to cover approximately 90 days of import-dependent consumption. European nations adopted similar measures, complemented by policies aimed at reducing oil dependency through energy efficiency, nuclear energy development, and the diversification of oil suppliers. In quantitative terms, OECD countries collectively increased their oil inventories by over 50% between 1973 and 1980, a clear reflection of the lessons learned from the supply disruption. Moreover, the crises prompted policymakers to boost early subsidies to clean technologies. For instance, the Danish government to introduce subsidies for wind turbines and set attractive electricity tariffs, creating a robust local market for early Vestas machines.

Stagflation Trends

As a result, industrial sectors that were heavily energy-intensive, including steel, chemical manufacturing, and transportation, faced escalating costs that were often passed on to consumers. In the United States, real GDP growth slowed from 5.6% in 1973 to 3.2% in 1974, while inflation rates peaked at over 11%. Europe experienced similar stagflation patterns, a phenomenon characterized by the simultaneous occurrence of high inflation and stagnating growth - a pattern previously thought to be economically impossible.

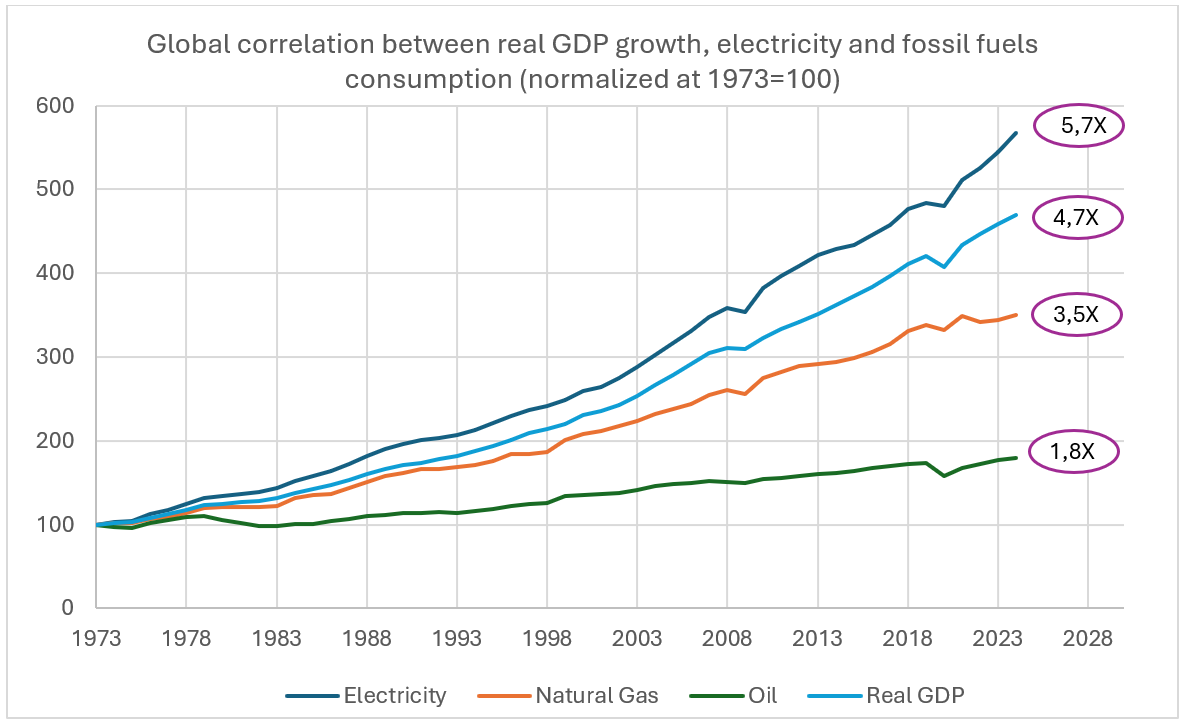

As data illustrate in Figure 2, a profound structural decoupling between global economic output and hydrocarbon dependency can be observed, a shift fundamentally catalyzed by the 1973 and 1979 oil crises. These exogenous shocks terminated the era of linear correlation between wealth and crude oil, forcing a permanent collapse in oil intensity as advanced economies prioritized energy security, fuel substitution, and radical efficiency gains. While Real GDP has expanded by a factor of ~4.7 since the initial crisis, oil consumption has exhibited significantly lower growth, reflecting a fundamental shift in the macroeconomic production function away from carbon-heavy inputs.

In contrast, electricity consumption has emerged as the dominant vector of modernization, consistently overarching GDP growth as the global infrastructure undergoes systemic electrification and digitalization. Natural gas has maintained a resilient role as a "transitional bridge," exhibiting a growth profile that tracks more closely with economic expansion than oil, yet failing to match the exponential trajectory of the electric sector. Ultimately, the widening "efficiency jaw" between these indices confirms that the 21st-century economy has transitioned from a framework powered by physical fuel combustion to one underpinned by high-density electrical and electronic throughput with regards to the latter, this will give further rise to global energy consumption from data centers.

![]()

Figure 2: Correlation between real GDP growth, electricity and fossil fuels primary energy consumption (normalized at 1973=100) – sources: World Bank Open Data, IMF, IEA World Energy Balances, United Nations Energy Statistics Yearbook, Energy Institute (EI) - Statistical Review of World Energy

Beyond the immediate concerns of price volatility, energy security encompasses the diversification of supply, the robustness of infrastructure, and the capacity for rapid adaptation to crises. The 1973 shock catalyzed an era of investment in energy efficiency technologies, alternative fuels, and nuclear power. As a result, between 1973 and 1980, energy intensity - measured as the ratio of energy consumption per unit of GDP - declined by approximately 10% in OECD countries. These improvements were achieved through industrial process optimization and thermal efficiency upgrades. In subsequent decades, Europe also accelerated the adoption of renewable energy sources, with wind and solar capacities increasing exponentially after 2000. By 2020, renewables accounted for nearly 20% of the EU’s gross electricity generation, illustrating a long-term structural shift partially motivated by the vulnerabilities highlighted in 1973.

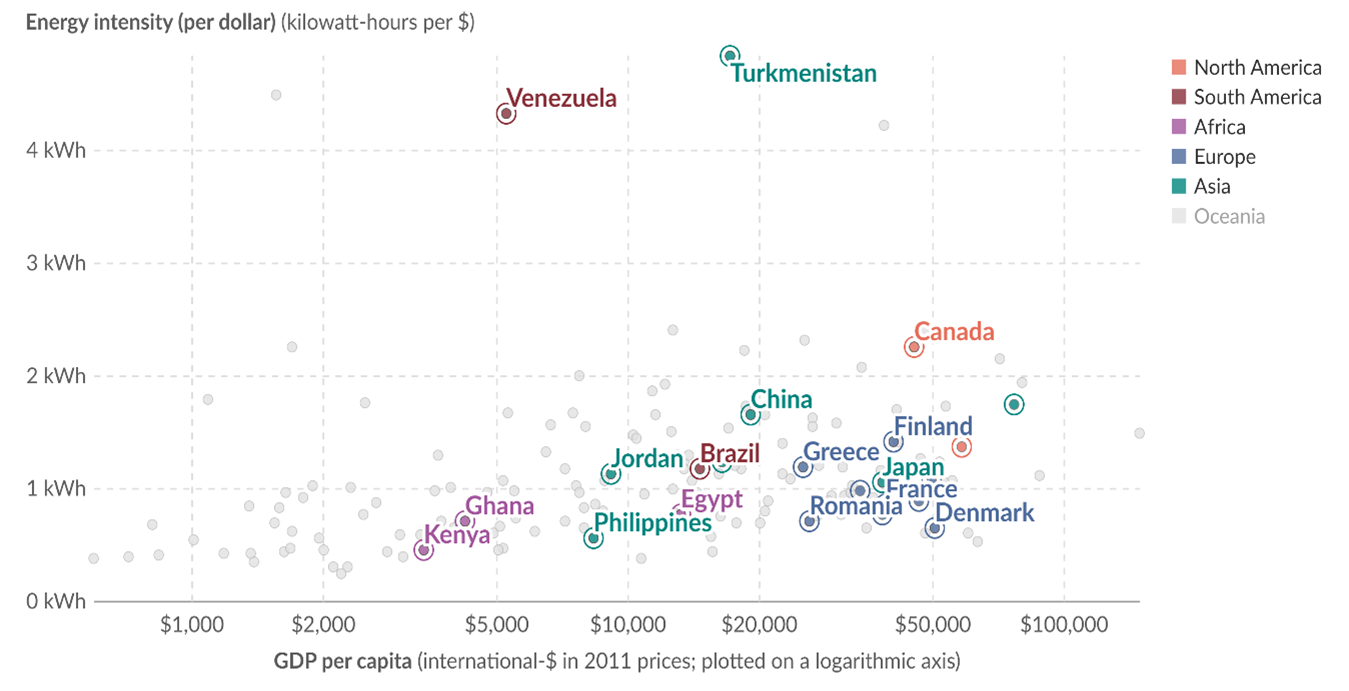

The decoupling of value creation in an economy from fossil fuel consumption is also showcased from the following figure. Advanced economies like Denmark and Germany have moved to the far right (high wealth) and far bottom (high efficiency), proving that "electronic throughput" is far more productive than the "fuel combustion" framework of the 1970s. In contrast, the outliers at the top, like Turkmenistan and Venezuela, represent a stagnated industrial model where energy is wasted as heat rather than converted into digital or service-based economic growth.

![]()

Figure 3 Energy intensity vs. GDP per capita in 2022 – source: Our World in Data, U.S. Energy Information Administration, Energy Institute - Statistical Review of World Energy

The 1973 oil crisis also illuminated the importance of international cooperation and shared risk management. While national stockpiles provided immediate relief against supply shocks, the creation of supranational mechanisms, including the International Energy Agency and coordinated emergency response protocols, institutionalized a form of collective security previously absent in global energy markets. Today, similar principles apply to the European Union’s approach to energy resilience. Tools such as the EU Gas Coordination Mechanism, cross-border interconnections, and regional energy hubs are designed to allow flexible redistribution of energy in response to localized disruptions, echoing the post-crisis lessons that no nation can be fully insulated from global energy shocks.

In recent years, energy security challenges have been compounded by the imperative of sustainability. The energy crises of the 1970s and early 2000s primarily focused on supply disruption and price volatility. Contemporary policy, however, integrates climate considerations, necessitating a dual focus on reliability and decarbonization. The European Green Deal, for instance, links energy security with ambitious targets to reduce carbon emissions by 55% by 2030 relative to 1990 levels. These policy frameworks inherently modify the risk landscape: supply disruptions from oil or gas now interact with renewable intermittency, grid stability requirements, and the economic feasibility of low-carbon alternatives. Investments in interconnectors, smart grids, and energy storage technologies represent quantitative manifestations of this approach. For example, the EU plans to invest approximately €30–40 billion in energy storage and interconnection projects between 2025 and 2030, reflecting both a strategic and financial commitment to resilience.

The lessons from historical crises like 1973 remain highly instructive. First, concentration risk in energy supply routes and sources amplifies the impact of geopolitical events. Second, proactive infrastructure investment - including strategic reserves, diversification of suppliers, and technological modernization - mitigates the economic consequences of shocks. Third, regional and international coordination magnifies the effectiveness of individual policies, allowing for collective absorption of disruptions. Finally, the integration of sustainability objectives into energy security planning ensures that resilience is compatible with long-term environmental and societal goals, avoiding the pitfall of short-term fixes that exacerbate systemic vulnerabilities.

The Strait of Hormuz, Geopolitical Chokepoints and Systemic Risk

Oil Market Disruptions

According to IEA data, a hypothetical 10% reduction in global oil supply - roughly equivalent to a major disruption in the Persian Gulf - could result in price increases exceeding 50% in the short term, with GDP growth reductions of 0.5–1.5% in major importing economies. Historical precedent from 1973 and 1979 suggests that these effects are asymmetric: developing economies with limited financial buffers suffer disproportionately, while energy exporters benefit from windfall revenues, often exacerbating global imbalances.

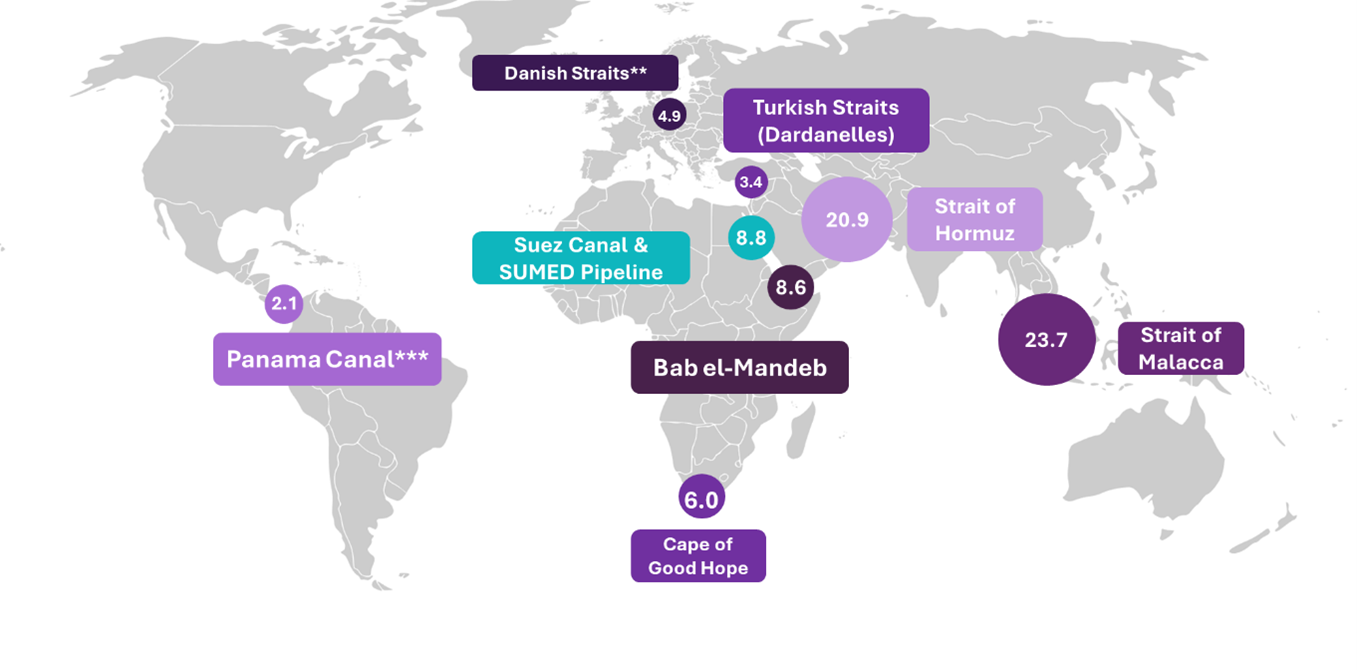

Strategically, the Strait of Hormuz exemplifies the interaction between geography and global energy stability. Maritime chokepoints - as illustrated in Figure 3 - reveal a narrow corridor connecting the Persian Gulf, home to over 60% of the world’s proven oil reserves, to open waters leading to Asia, Europe, and the Americas. Alternative routes, such as the United Arab Emirates’ Habshan–Fujairah pipeline or the Saudi East–West pipeline, offer partial redundancy but cannot fully substitute for the throughput capacity of the strait. Consequently, energy security planning must incorporate scenario analyses, including partial and complete closures, with quantitative modeling of price impacts, supply reallocation, and secondary market effects.

![]()

Figure 4: Volume of crude oil and petroleum liquids transported through world chokepoints* in 2023 (million barrels per day), source – source: EIA

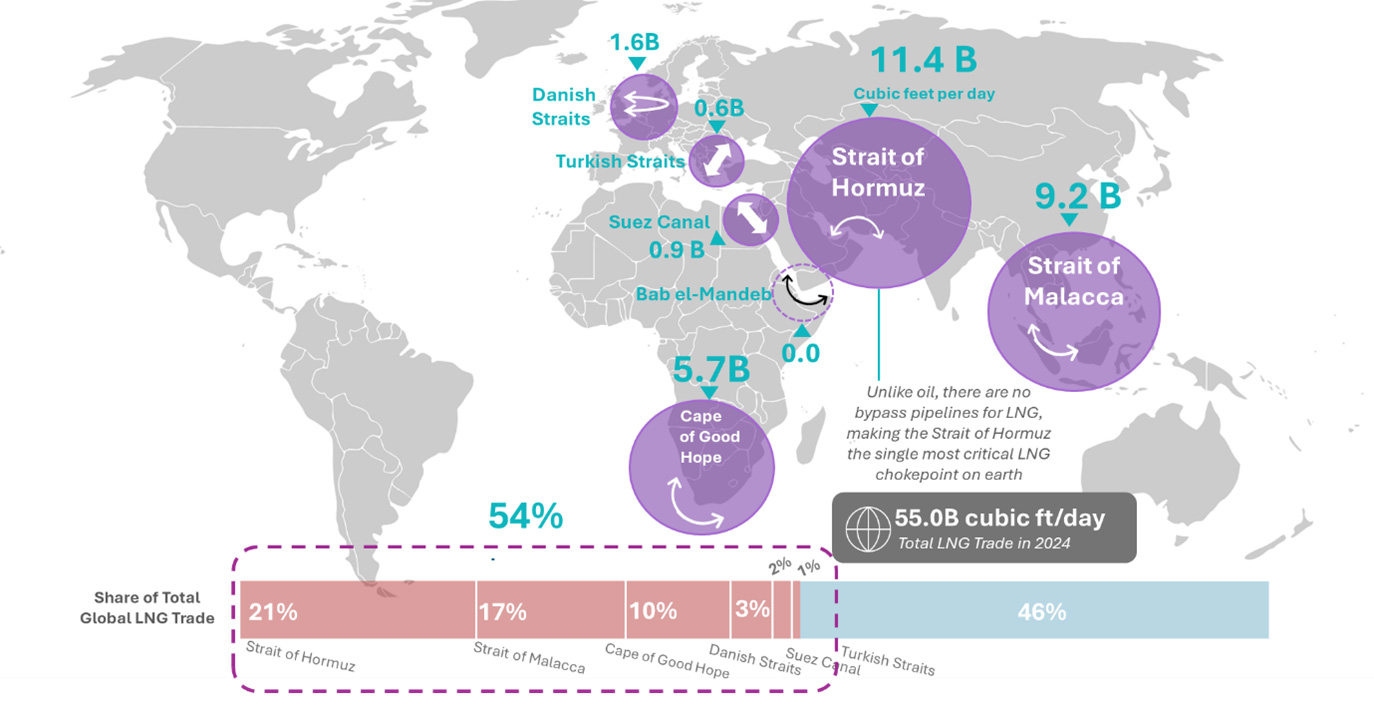

Figure 5 illustrates the primary chokepoints for global LNG shipments, showing both volume and geographic concentration. It demonstrates how LNG trade - like oil - relies on a limited number of strategic corridors, making the gas market similarly exposed to geopolitical or physical disruptions.

![]()

Figure 5: Volume LNG transported through world chokepoints (billion cubic feet) - source: EIA, World LNG Report

From Physical Disruption to Price Volatility

While historical energy security concerns were centered on physical supply disruptions, modern energy systems are increasingly exposed to price volatility transmitted through global fuel markets, particularly natural gas.

As electricity markets evolved toward marginal pricing, this exposure became more pronounced. Gas-fired generation typically set the wholesale electricity price, meaning fluctuations in global gas benchmarks directly translate into power price volatility. In this context, energy security is no longer only about access to resources, but also about limiting exposure to external price shocks.

From an energy security perspective, the increased RES deployment (assuming timely deployment of transmission grids and flexibility sources such as demand response, storage) contributes apart from decarbonisation, to enhanced energy security, market stability and reduced exposure to fossil fuel price volatility during extreme events, as reflected in lower wholesale electricity prices during periods of high renewable output.

The role of energy transition: From Sustainability to Security

Historically promoted for environmental reasons, RES now contribute directly to energy security through multiple mechanisms. First, by displacing fossil fuel–based generation - particularly natural gas - renewable energy sources (RES) reduce dependence on energy imports – particularly imported fossil fuels, thereby enhancing both economic and geopolitical resilience. Second, because RES operate at near-zero marginal cost, their generation lowers the frequency with which high-cost gas-fired plants set electricity market prices, helping to dampen price volatility during extreme events. Third, a more diversified generation mix reduces systemic risk by decreasing reliance on single fuels or external suppliers.

However, the integration of RES also involves several transition challenges, including intermittency, the need for energy storage, and enormous grid infrastructure needs, which must be carefully managed to maintain reliability and stability. Thus, in order to properly compare costs along the entire value chain a more holistic approach needs to be followed including the cost of grids, storage, capacity mechanisms to ensure viability of CCGTs, flexibility etc.

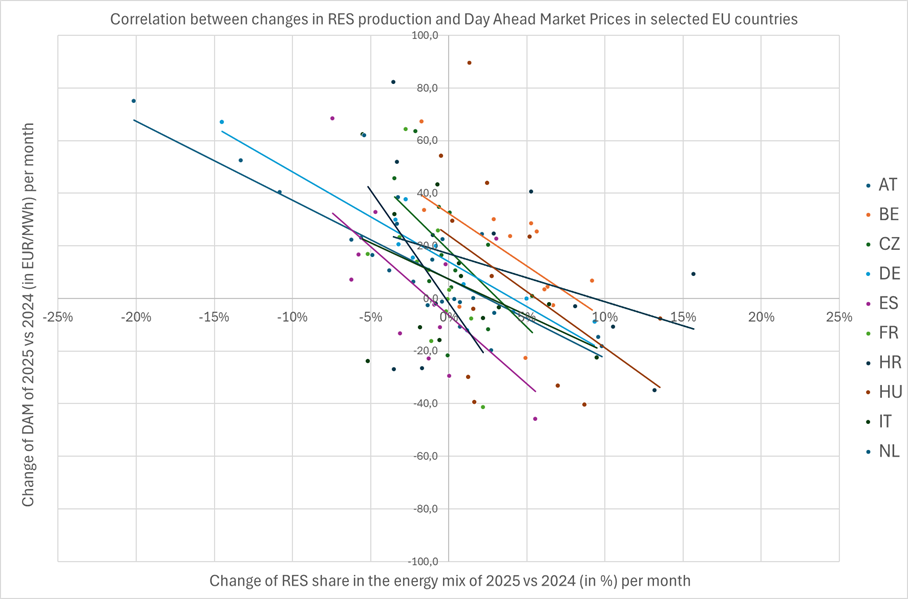

The role of RES in decreasing energy prices can be easily showcased by empirical data. The figure below illustrates the correlation between monthly changes in RES share in the generation mix and corresponding changes in day-ahead electricity market prices across selected European countries. Each point represents a monthly observation (Δ in RES share in the generation mix of 2025 vs 2024 and prices respectively), while the straight lines indicate country-level trends (linear).

![]()

Figure 6: Relationship between changes in RES share in the generation mix and Day-Ahead Market (DAM) prices across selected EU countries (2025 vs 2024) – source: ENTSOE Transparency platform, own elaboration.

Overall, the figure reveals a consistently negative relationship between RES generation and electricity prices. In most countries, increases in RES generation are associated with reductions in DAM prices, whereby low marginal-cost renewable generation displaces more expensive conventional generation - primarily gas-fired units. The strength and slope of this relationship vary across countries. Markets with higher structural RES penetration or greater system flexibility (e.g. interconnections, hydro capacity) tend to exhibit a more pronounced price dampening effect, as seen in steeper downward trend lines. Conversely, in systems with tighter supply conditions or grid constraints, the impact appears more moderate and dispersed. The dispersion of data points around the trend lines highlights the influence of additional factors beyond RES generation, including fuel prices (which were quite comparable in 2025 vs 2024), demand fluctuations, cross-border flows, and weather conditions determining demand. Nevertheless, the overall pattern remains robust across the sample.

Conclusion

Strategic Takeaways

The evolution of energy security from the oil shocks of 1973 till present reflects a fundamental shift. Geopolitical chokepoints such as the Strait of Hormuz remain critical, while modern vulnerability is reflected through price volatility and systemic exposure to global fuel markets. Thus, a constant diversification of fuels and routes is always a strategic priority.

RES structurally reduce both import dependence and price exposure to fossil fuels. By limiting the influence of volatile gas markets on electricity prices, RES enhance the resilience of modern energy systems. Nevertheless, in order to for RES to play such a crucial role, transmission and distribution grids need to be developed, flexibility resources - including flexible thermal units – need to be present in the and markets need to be reformed to ensure a smooth decarbonisation pathway.

Energy security in the 21st century is therefore no longer defined solely by access to resources, but by the flexibility, constant diversification, and composition of the energy system itself.

Related Services

We work at an impressive pace. Yours. Discover how: